$8.5bn worth of deals mark the UK’s post-Brexit investment plans for Africa

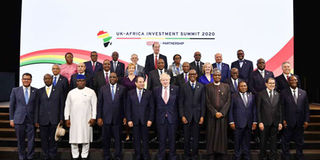

British Prime Minister Boris Johnson with African presidents and government representatives, and World Bank, IMF and UN officials at the start of the UK-Africa Investment Summit in London on January 20, 2020. PHOTO | AFP

There were pledges for $1.9 billion (£1.5 billion) worth of initiatives for sustainable infrastructure, targeting private sector investments and drawing them to fund road, energy, ICT and other infrastructure projects in Egypt, Ethiopia, Ghana, Kenya and Uganda.

Kenya also secured a pledge for partnership in cancer research after the University of Manchester Hospital and Christie National Health Service Foundation inked MoUs on a Cancer Research Centre.

The UK this past week opened a new chapter in its relations with African countries at a summit to set the tone for the country’s trade and diplomatic ties with the continent after exiting the European Union.

British Prime Minister Boris Johnson hosted leaders from 21 African countries in London, where 27 deals worth an estimated $8.5 billion (£6.5 billion) were signed at the UK-Africa Summit held on January 20.

The summit came just months after Japan and Russia hosted African leaders in their respective capitals last year.

“We want to build a new future as a global free trading nation, that’s what we are doing now and that’s what we will be embarking on, on 31st of January,” Mr Johnson told the gathering in London. “But I want to intensify and expand that trade in ways that go far beyond what we sell you or you sell us.”

The tone of the meeting signalled a shift in Mr Johnson’s attitude towards Africa. Eight years ago, as mayor of London, he wrote a commentary in the Spectator Magazine suggesting that Africa would have been better off if the UK was still its colonial master.

Britain expects to start an 18-month transition from being a member of the EU beginning January 31, to being an independent country capable of signing bilateral or multilateral trade deals. Britain may have to renegotiate all trade deals initially signed under the EU, including with African countries.

In the EAC, for example, Britain had been a part of the EU’s negotiations for the Economic Partnership Agreements, which determined how to tax goods or exempt them from any levies.

In the EU transition period, some government officials in Kenya say the two sides should reach a quick deal to avoid falling into a vacuum once the 18-month transition ends.

At the Summit, KEFI Minerals, a precious metals exploration firm, announced it would invest $293 million (£224 million) in a new gold mine and to develop local infrastructure in Ethiopia.

Green energy company Nexus Green said it would be exporting $104 million (£80 million) of solar-powered water pumping systems to be used for irrigation in Uganda.

Solar power producer Globeleq said it would invest $59 million (Ksh6.6 billion) in establishing a solar farm in Malindi at Kenya’s Coast.

Troubled British exploration firm, Tullow Oil, was also listed as having pledged to continue investing $1.5 billion (£1.2 billion) in continued oil production in Kenya.

British beer maker Diageo, which owns a large part of East African Breweries Ltd, also made a big announcement. The global brewer said it would invest $218 million in projects to reduce its impact on the environment by running factories that recycle and also emit less harmful wastes.

“I am glad that in his speech, the Prime Minister indicated that our products, including Uganda's beef, would find its way onto the dining tables of post-Brexit Britain. Our position has always been balanced trade that benefits all parties,” said Uganda’s President Yoweri Museveni. “Like I told him in our bilateral meeting, Uganda is ready to receive British investors, given the immense business opportunities in the Pearl of Africa.”

There were pledges for $1.9 billion (£1.5 billion) worth of initiatives for sustainable infrastructure, targeting private sector investments and drawing them to fund road, energy, ICT and other infrastructure projects in Egypt, Ethiopia, Ghana, Kenya and Uganda. Kenya also secured a pledge for partnership in cancer research after the University of Manchester Hospital and Christie National Health Service Foundation inked MoUs on a Cancer Research Centre.

“We had a great summit. Great focus on economic prosperity underpinned by a new strategic partnership agreement,” said Kenya’s High Commissioner to London Manoah Esipisu, referring to agreements signed between Kenya and the UK.

Kenya listed a $40 million green bond on the London Stock Exchange, intended to finance real estate projects.

For the UK though, the pledges came amid serious criticism of how it sees Africa. Beaten to the game by the Chinese and with stringent immigration rules for Africans, critics have argued that UK’s influence on the continent may take a while to rise again.

Mr Johnson did acknowledge the competition. “There is no shortage of governments out there touting for your business. China, I must mention the competition, I better I mean why not, China, Russia, Germany. I’m told there will be a conference in France fairly soon,” he said, referring to the upcoming France-Africa Summit set for January 31 in Paris.

“But in the words of an old Akan proverb that I picked up while I was in Ghana, ‘All fingers are not the same’. There is wisdom in these Akan proverbs. All fingers are not the same and all countries are not the same, and the UK boasts a breadth and depth of expertise that simply cannot be matched by any other nation.”

UK’s recent interest in Africa rose especially under Theresa May, the immediate pro-Brexit prime minister. In 2018, she toured Nigeria, Kenya and South Africa where most of UK investments are centred on the continent.

The Overseas Development Institute (ODI), a British think-tank, this past week said the UK may need to diversify its focus on the continent, and put more money in other sectors away from the usual financial services and the extractive industry.

In 2017, the UK was the fourth-largest investor in Africa, behind China and India. But most of that money went to the banking sector, oil extraction and mining of metals.

ODI says information provided by more than 75 UK companies operating in Ghana, Kenya, Nigeria and South Africa shows that banking and mining were the main focus of investment.

“The low penetration of UK FDI beyond mining and financial services and in other countries suggests that there are opportunities as well as challenges to increase the role of British investors in boosting African economies,” ODI experts Max Mendez-Parra, Sherillyn Raga and Lily Sommer said.

The UK sent 4.3 per cent ($1.2 billion, £897 million) of its total FDI in Africa to Kenya in 2018. Some 67 per cent of this money went to the services sector, 37 per cent to manufacturing, four per cent to agriculture and just one per cent to the extractive industry. UK’s total investment into Kenya that year was $790 million (£532 million).

“Investment concentration on this sector is not necessarily desirable. Oil resources are vulnerable to international price shocks, putting the growth path of resource-rich countries at risk,” ODI says in the report titled Africa and the United Kingdom: Challenges and Opportunities to Expand UK Investments.

The establishment of Special Economic Zones, particularly in Kenya, say the experts, and more regional collaboration could influence British firms to diversify.