Local African institutions edging out foreign bank subsidiaries

Local banks, now fast expanding into regional operations, as well as others that are pan-African, are driving the development of Africa’s banking industry.

What you need to know:

Banking experts argue that lending to small and medium enterprises (SMEs) has been part of the reason for the success of African banks.

In East Africa, despite coming at the bottom of the ladder among emerging African banking groups, Kenya Commercial Bank (KCB) leads the pack of homegrown brands followed by Equity Bank and I&M Group at $1 billion.

Local banks’ flexibility is in the lower borrowing threshold they offer their customers as opposed to foreign banks’ lending threshold, which is as high as $7,807.

Currently, Africa’s banking sector is the most profitable in the world.

Over the past decade, homegrown banks — led in East Africa by Kenyan brands — have eroded the market share of the traditional big boys of the industry, largely Western transnationals.

These local banks, now fast expanding into regional operations, as well as others that are pan-African, are driving the development of Africa’s banking industry.

Coming against a backdrop of hardships that local banks suffered in the 1990s, the expansion is a major coup against Western banking groups, most of which started operations on the continent during the colonial era.

The most dominant foreign banks in Africa have been Standard Chartered, Barclays, and Citibank, focusing on the corporate consumer segment in Anglophone countries; French giants BNP Paribas and Societe Generale have ruled Francophone West and North Africa.

But the tide is turning, with local banks slowly taking over the industry in Africa, a scenario that offers attractive investment opportunities for banking models suited to Africa’s business terrain — lending to the small retail client involved in cross-border trade.

In the 16th edition of Private Sector and Development magazine, published by French lending group Proparco, banking experts argue that lending to small and medium enterprises (SMEs) has been part of the reason for the success of African banks.

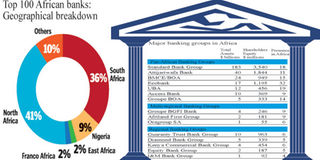

“Foreign bank subsidiaries have gradually lost their dominant position — probably permanently — to African banks. The new leaders, which are few in number, come from several countries. Morocco and Nigeria have the most extensive networks, followed by South Africa and, more recently, Kenya and Gabon,” said Paul Derreumaux, former chief executive officer of Bank of Africa, one of the most visible banking groups on the continent, with a presence in 14 countries.

In East Africa, despite coming at the bottom of the ladder among emerging African banking groups, Kenya Commercial Bank (KCB) leads the pack of homegrown brands, with total assets of $4 billion, and a presence in Kenya, Uganda, Tanzania, Rwanda, South Sudan and Burundi.

KCB is followed by Equity Bank at $2 billion worth of assets, with a presence in five countries, and I&M Group at $1 billion, operating in three countries.

Experts at Proparco say these Kenyan banks, which account for just two per cent of the continent’s banking industry, are still restricted to one region, but the fact that they feature among the giants of Africa’s banking models shows their growing financial muscle.

“A number of local commercial banks have successfully expanded regionally. They differ from the international banking groups in a number of ways. These include flexibility and leveraging technology to service customers. They focus on retail and on growing SMEs, building loyalty among their customers,” said Sarit Raja Shah, chairman of I&M Tanzania and director of Bank One.

Local banks’ flexibility is in the lower borrowing threshold they offer their customers as opposed to foreign banks’ lending threshold, which is as high as $7,807.

Risk factor exaggerated

Western investors say getting into any industry in Africa, especially banking, which lacks financial infrastructure and security guarantees, is too risky.

However, the banking sector in Africa has remained profitable in spite of social and political crises. For example, profitability remains high, with average return on equity for Kenyan banks at 20 per cent, despite the post-election crisis of 2007-08.

“Ability to bounce back shows that African economies are highly resilient to this type of crisis. Profits are volatile, but the rebound effect compensates for periods of poor performance. This guarantees record returns on investment in Africa for investors who take a long term view and are able to diversity their assets geographically,” said Proparco executives Laureen Kouassi-Olsson and Julien Lefilleur.

The African banking model is all too aware of the political risks, hence the strategy to expand regionally.

“A bank will more easily absorb the shock of political and social instability if it has a presence in other countries. The 2007-08 post-election crisis in Kenya is a good reminder how quickly a situation can deteriorate and impact the economy. If a bank is too small, and only local, such a crisis can threaten its existence,” said Mr Shah.

Yet for all the negativity, the degree of risk in Africa is often exaggerated. Ms Kouassi-Olsson and Mr Lefilleur argue that the sensitivity of foreign banks to Africa’s risk factors outstrips their awareness of the profits that can be achieved.

Currently, Africa’s banking sector is the most profitable in the world. Between 2007 and 2010, average return on equity in Africa was 19 per cent, compared with 11 per cent in Europe. This was despite the higher capitalisation levels of African banks.

Very few foreign banks — either from the developed world or the developing markets of China and India, which are Africa’s main trading partners — have sought to establish a presence in sub-Saharan Africa (excluding South Africa) in the past 30 years. The Bank of India’s return to Uganda last year, after a 40-year hiatus, is an isolated case.

Allure of regional markets

Still, for the African banking model, the desire to grow regionally and thereby spread risk, is attracting more local players. One of these is Uganda’s Crane Bank, whose expansion into the region would make it the first Ugandan bank to do so.

“We are going regional with branches in Rwanda and DR Congo. We’ve secured the licence in Rwanda, to start operations on January 1, 2014. In Congo, we’ll wait for the country to stabilise. We are also looking at South Sudan,” the bank’s managing director A.R. Kalan, told The EastAfrican.

Despite its operations being restricted to one country, Crane Bank is profitable. Founded in 1995, and with assets of $345.2 million, it was ranked top in 2011, by The Banker magazine, among the lenders with the highest return on assets globally, at 8.70 per cent.

But all has not always been well. Towards the turn of the last century, local commercial banks in several African countries struggled to stay solvent, and suffered the ignominy of closure by their central banks.

In 1998, an Unctad study on Africa’s banking industry said the causes of financial distress had to do with the low minimum capital requirement to start a bank — $50,000 in Uganda and Zambia at the time. Central banks have since become stricter in their regulations.

But more critically, banks in Africa have struck up a relationship with development financial institutions (DFIs) in Europe to mobilise capital and bolster their financing capacities.

For instance, from the time Proparco started lending to local African banks, about 25 years ago, lines of credit have provided resources for lending to SMEs, and in turn driven African economies in job creation and contribution to gross domestic product.

“African banks have limited resources and need to partner with financial investors. In this process, DFIs have a role to play. In recent years, DFIs have been supportive of banks by taking equity and providing senior debt,” said Mr Shah, citing Kenya’s I&M Group whose expansion into Rwanda and Tanzania was supported by Proparco and German funder DEG.

Multinational banks, which rely on their parent companies to finance or syndicate large transactions, usually compete for large clients whose needs exceed the financing capacities of the average African bank. The options for African banks therefore are to raise resources locally — which is difficult — or seek help from DFIs.

As they partner with financing groups for regional expansion, another opportunity for African banks arises. According to Private Sector and Development, the penetration rate of Africa’s banking sector is around 30 per cent — less than half the average in other developing nations — an opportunity for growth, provided the banks have the resources to keep lending.

Because of this need, DFIs’ participation in the African financial sector includes interventions like equity investments, credit lines, and guarantees to the private sector. As of December 2012, Proparco’s financial sector portfolio to Africa stood at $938 million.

With support from DFIs, a trusted client base and a robust retail model, pan-African banks such as Ecobank, Bank of Africa, Standard Group and United Bank of Africa are giving foreign-owned banks a run for their money.

Standard Chartered and Barclays are seeking new customers in previously neglected retail and SME market segments, and even offer unsecured salary loans.

Multinationals are now playing catch-up with local banks by lending to riskier customers on flexible lending terms. Local banks have stimulated competition and boosted lending activity in Africa over the past decade, Ms Kouassi-Olsson and Mr Lefilleur say.

In contrast to the 1990s when loans to the private sector in Africa remained at around 10 per cent of GDP, the new banking models, spearheaded by KCB, Equity, Standard Group, I&M, Ecobank, Bank of Africa and UBA, have taken the loans up to 20 per cent of GDP.

Trust has been built between the banks and their customers. Local banks offer trade financing to export markets in the region; and others lend to women in urban areas who are into all manner of economic activities.

This is why local banks attract long term financing from DFIs — to foster lending to the retail borrower, and enable local banks to support long term credit facilities.