Mobile money subscribers on the rise across the region

East Africans are now using mobile money platforms to move cash equivalent to a third of the value of goods and services produced in the region, the latest industry statistics show. TEA GRAPHIC |

What you need to know:

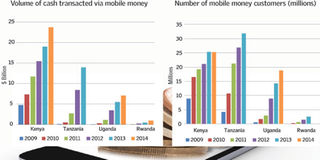

Consumers in Kenya, Uganda, Rwanda and Tanzania last year transacted $45.75 billion through their mobile phones — translating into 32 per cent of their combined gross domestic product — up from $4.86 billion or 3.4 per cent of GDP in 2009.

There are 24 mobile money service providers across the EAC; Safaricom’s M-Pesa is ranked the biggest, with 20.63 million registered customers as at March.

Mobile money is also seen as a tool for connecting social networks in East Africa, allowing families and friends to share and absorb financial shocks through remittances, researchers say.

Mobile money has evolved beyond cash transfers to include payment of utility bills (such as water, rent and electricity), shopping, receiving dividends, diaspora remittances and paying government taxes.

East Africans are now using mobile money platforms to move cash equivalent to a third of the value of goods and services produced in the region, the latest industry statistics show.

Consumers in Kenya, Uganda, Rwanda and Tanzania last year transacted $45.75 billion through their mobile phones — translating into 32 per cent of their combined gross domestic product — up from $4.86 billion or 3.4 per cent of GDP in 2009.

The annual growth in volumes means that East African consumers are moving an average of $3.8 billion monthly or $125 million per day compared with the $13.3 million a day they transacted five years ago.

The number of registered mobile money subscribers across the four countries was 82.3 million as at December last year, up from 29 million customers in 2009.

There are 24 mobile money service providers across the EAC; Safaricom’s M-Pesa is ranked the biggest, with 20.63 million registered customers as at March.

Zimbabwe is the only country outside East Africa with a successful mobile cash industry, grossing $3.6 billion in mobile cash in 2014 – about a quarter of GDP – according to data from the Reserve Bank of Zimbabwe.

Leora Klapper, a lead economist at the World Bank and co-author of the 2014 Global Findex, said consumers are increasingly using mobile money because the platform is faster, more efficient, safer and more transparent than using cash.

“It has reduced risks like leaky transfers, delays and high cost of transactions for users who want to transfer money to family members and friends,” Dr Klapper said.

Mobile money is also seen as a tool for connecting social networks in East Africa, allowing families and friends to share and absorb financial shocks through remittances, researchers say.

“This means greater opportunities for women to find funds for keeping a small business going, keeping children in school, and dealing with medical and other emergencies,” said Dr Klapper.

The growth of mobile cash in East Africa caught the eye of US President Barrack Obama, who hailed SMS-based financial transactions as a great innovation that helps power businesses.

“Millions of people send and save money with M-Pesa — and it’s a great idea that started here in Kenya,” President Obama said at the Global Entrepreneurship Summit held in Nairobi in July.

Mobile money has evolved beyond cash transfers to include payment of utility bills (such as water, rent and electricity), shopping, receiving dividends, diaspora remittances and paying government taxes.

Mobile phones are now used to provide access to financial services, especially for those locked out of the formal banking system.

“Mobile money has been growing at a dizzying rate. Mobile money is transforming the way people access financial services,” researchers at London-based GSMA said in a report.

“Traditional ‘bricks and mortar’ banking infrastructure struggles to make the business model work to serve low-income customers, particularly in rural areas,” the association added.

Kenya — the cradle of mobile money, where M-Pesa was launched in March 2007 — posted a nearly fivefold growth in volumes in as many years to hit $23.7 billion last year; about 39 per cent of GDP.

Ugandans transferred $7.14 billion through mobile phones in the year 2014 while Rwandans moved $0.96 billion from their cellphones over the same period, corresponding to 27 per cent and 12 per cent of GDP respectively.

Tanzania moved $13.9 billion in 2013 — the latest data available — which is equivalent to 28 per cent of its GDP.

Kenya is ranked the biggest economy in East Africa with a GDP of $60.94 billion followed by Tanzania ($49.18 billion), Uganda ($26.31 billion) and Rwanda ($7.89 billion), according to a World Bank statistical database dated July 2015.

British telco Vodafone — which owns a 40 per cent stake at Safaricom and a further 82.2 per cent in Vodacom Tanzania — said the continued growth of mobile money is attributed to the fact that it services consumers at the bottom of the pyramid who cannot access banking services.

“It is not enough to persuade unbanked customers to start using a bank account, nor does it overcome the hurdles that frequently deter customers from having a bank account — price structure, availability and trust. Mobile money addresses these issues,” a spokesman at Vodafone said.

Customers are also wooed to mobile money due to its extensive network of agents, and the frequent addition of innovative financial products such as micro-insurance, mobile loans and savings accounts.

“Mobile telecommunications infrastructure is more reliable and extensive than the banking infrastructure,” said Stephen Rea, a research assistant at the Institute for Money, Technology and Financial Inclusion at the University of California, Irvine.

“People adopt whichever services make the most sense for them,” he said in an interview.

Widespread

The World Bank 2014 Global Findex report says that mobile money is most widespread in East Africa, where one in every five adults has a mobile money account.

Kenya tops the globe with the highest number of adults with a mobile money account, at 58 per cent, followed by Somalia’s 37 per cent thanks to its well-entrenched mobile-based Hawala system; Uganda is at 35 per cent and Tanzania 32 per cent.

About eight out of every 10 Kenyan adults are banked — through banks and mobile money accounts — ahead of Uganda’s 44 per cent, Rwanda’s 42 per cent, Tanzania’s 40 per cent, and Burundi’s seven per cent.

Cross-border mobile money remittances and retail payments for school fees, agricultural products and payment of wages via mobile cash are now seen as the next frontier in the mobile money industry.

“Providers are now serving a growing number of verticals such as retail merchants, utility companies, governments and other third parties using mobile money as a payment channel,” GSMA said.